The crypto industry will only benefit from regulation

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

Since the emergence of Bitcoin in 2009, cryptocurrencies have become widespread. By 2022, the market included at least 10,000 tokens with various properties: well-known mainstream coins like Bitcoin and Ethereum, stablecoins with a value pegged to fiat currencies, meme coins, and various altcoins that power different projects.

Cryptocurrencies provide options for fast and inexpensive money transfers (including cross-border ones), have limited use for payments, and can be used as a store of value if not considering extreme volatility. However, the most common use for cryptocurrencies is speculation: the market has many players, from individuals to hedge funds, aggregating billions of dollars worth of crypto assets.

Crypto enthusiasts promote blockchain-based projects as alternatives to the traditional financial system with no need for intermediaries to hold and transfer one’s funds. Hence, the lack of a regulatory framework is considered a privacy-preserving feature. However, it comes with a price: investors in crypto projects are not protected at all, while the lack of regulation over crypto wallets and transfers made it a tool of choice for all kinds of criminals and money launderers.

One reason to regulate: widespread fraud

Traditional markets are regulated for a reason. There are organizational requirements for public offerings, strict technological standards to ensure the secure transfer and storage of assets, and anti-money laundering and counter-terrorism financing compliance to prevent criminal money from entering the financial system.

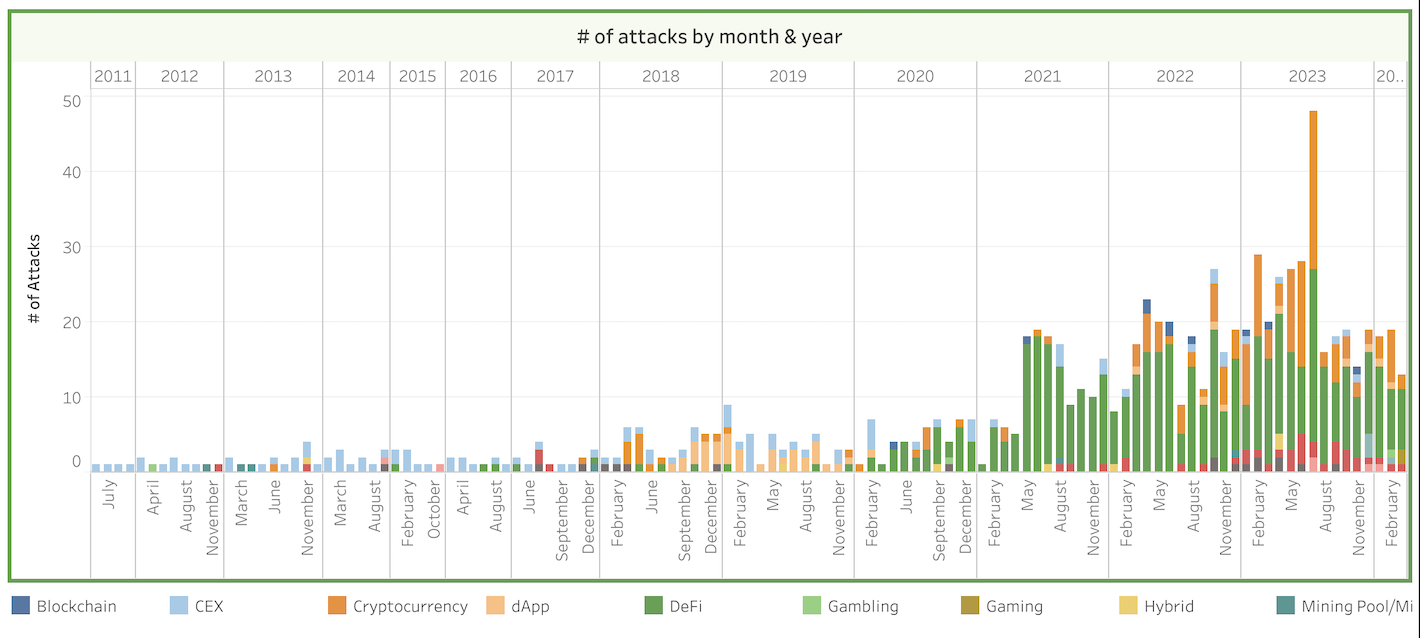

In the crypto industry, fraud is widespread. By 2024, the Worldwide Cryptocurrency Heists Tracker, which documents several types of cybercrimes, reported $10,5 billion in stolen crypto assets in 879 cases (which will roughly equal $50 billion in today’s prices). Those heists included exploits, hacks, flash loan attacks, reentrancy attacks (which utilize vulnerabilities in specific smart contracts), price manipulations, third-party attacks (which use the infrastructure of a partner), insider attacks, 51% attacks (such an amount of tokens effectively grants attacker direct control over the network), governance attacks (manipulating governance decisions).

Another project, dubbed Web3 is going just great, tracks rag-pulls (which also tracks rug-pulls when a developer simply disappears with investors’ money), employee fraud, and thefts from individuals recorded a whopping $72.5 billion lost to cryptocurrency scams. The list includes the Terra/Luna collapse and frauds committed by the founders of FTX, Bitconnect, Bitclub, OneCoin, etc. In most cases, fraudsters laundered the proceeds and disappeared without a trace.

Anonymity and privacy for money laundering

The crypto community typically blames traditional regulatory frameworks for ineffectiveness; however, it’s good enough to push criminals toward unregulated cryptocurrencies. They became the financial vehicle of choice for various fraudsters, underground gambling, drug trafficking, cybercrime services, selling of stolen goods, human trafficking, child sexual abuse and exploitation, murder for hire, and other kinds of crime.

Cryptocurrencies are anonymous by design and allow users to operate unlimited wallets (even though wallet addresses are the only public identification on the network). There are plenty of ways to obfuscate traces of crypto, such as decentralized exchanges, cryptocurrency mixers, side chains, chain hopping, and so-called privacy coins (which additionally conceal addresses and wallet balances of users), as well as crypto casinos and NFT. A combination of such instruments makes tracing a chain of transactions borderline impossible.

NFT is a prominent example of a market that developed and skyrocketed due to fraudulent techniques, such as rug-pulls, scams, insider trading, and wash trading (what one sells an asset to his own accounts to create an illusion of interest and pump the price). The ease of price manipulations made NFT a reliable instrument for money laundering. For instance, the largest NFT deal ever, the sale of CryptoPunk #9998 for $532 million in 2021, was quite possibly a mere attempt to launder money.

Criminals use non-custodial wallets (fully anonymized) and centralized exchanges with weak AML/CTF policies to launder money and finance illicit activities. In 2023, within a large-scale investigation, Binance admitted that it explicitly allowed money laundering on its platform and transactions connected to terrorist groups, such as Hamas, Al Qaeda, Palestinian Islamic Jihad, and the Islamic State of Iraq and Syria (ISIS). The company and its founder pledged guilty to criminal charges.

Are cryptocurrencies broken, and can they be fixed?

Cryptocurrencies can be convenient instruments for storing and transferring funds and risky but lucrative investment vehicles. Even though their distinctive qualities make them useful for criminals, most crypto users are law-abiding and good-faith people. A thought-out regulation won’t damage their interests but will probably facilitate the mass adoption of cryptocurrencies outside the tech-savvy community. The most obvious point in introducing regulations is the interconnection between the crypto industry and the traditional financial system (cryptocurrency exchanges, fintech apps, and more).

The cornerstone of the modern approach to combating money laundering is to prevent illicit money from entering the financial system, thus making it harder to put it into use. The first step is KYC, a basic identity check that helps to identify people with questionable backgrounds. It’s not a cure-all and can potentially be tricked with fake documents and sophisticated deepfakes; however, it’s compelling enough to drive away some criminals.

Another component of cryptocurrency regulations is the Financial Action Task Force’s (FATF) Travel Rule, which requires financial institutions and virtual assets service providers (such as cryptocurrency exchanges) to obtain information about the originator and beneficiary of the transactions and transfer them to other parties as the transaction occurs. This requirement initially applied to traditional finance; however, in 2019, the FATF extended this recommendation to virtual assets.

On-chain analysis can be another effective measure, as blockchain holds information about every transaction. However, as it is a complicated task that requires technology and expertise, it should be separate from compliance reporting.

Compliance is the key to mass adoption of cryptocurrencies

Many crypto enthusiasts believe that regulation itself goes against the spirit of cryptocurrencies and will hinder innovation. However, a lack of mass adoption limits crypto’s future development. For many, cryptocurrencies are also associated with illegal and semi-legal activities and speculation, and the banks are cautious about crypto due to compliance risks.

The EU was the first to apply the AML framework to crypto assets and is currently developing a unified set of rules for all member countries. The US slowly progressed towards crypto regulation. However, China took a restrictive stance on crypto. The real potential of cryptocurrencies heavily depends on integration with traditional finance, which in turn requires a well-developed and clever regulatory approach.